Find The Best Mortgage Rates in Kelowna,

British Columbia

5-year Fixed Rate

4.04%

High Ratio Mortgage

5-year Variable Rate

3.40%

Most Banks Current Prime Rate 4.95%

Get daily updated Canada mortgage lending rates from top lenders in Kelowna, British Columbia.

Speak with licensed mortgage brokers to secure the best mortgage rates and lowest mortgage rates in Canada on your terms.

Not Just the Best Mortgage Rate

With over 20 years of experience in the mortgage industry, we’ve been dedicated to helping Canadians save on their mortgage borrowing costs. We’ve seen it all and know what it takes to secure the best deals for you!

Your financial situation is unique—it’s your shelter, your home. That’s why we work tirelessly, negotiating with dozens of lenders across Canada to find you the best mortgage rates tailored to your specific needs.

Our team of experienced mortgage brokers is specially trained to identify opportunities within your income, credit, and assets. We build a strong case to present to our network of trusted lenders, ensuring you get the most competitive home loan rates in Canada.

Whether you’re looking for mortgage brokering services, broker mortgage loans, or simply the best mortgage rates in Canada, we’re here to guide you every step of the way. Let us help you make the most of your mortgage journey!

A Mortgage Solution, for Every Situation

Banks, Credit unions and branchless mortgage lenders compete with your bank's business.

Canadian Mortgage Lenders look for consistent volume business from RateShop brokers . As a Volume Brokerage, we get priority access to Rate Promotions, faster underwriting & approvals, lender exceptions and dedicated personnel are assigned to us to get you a better deal!

The Only Difference - You Save Thousands!

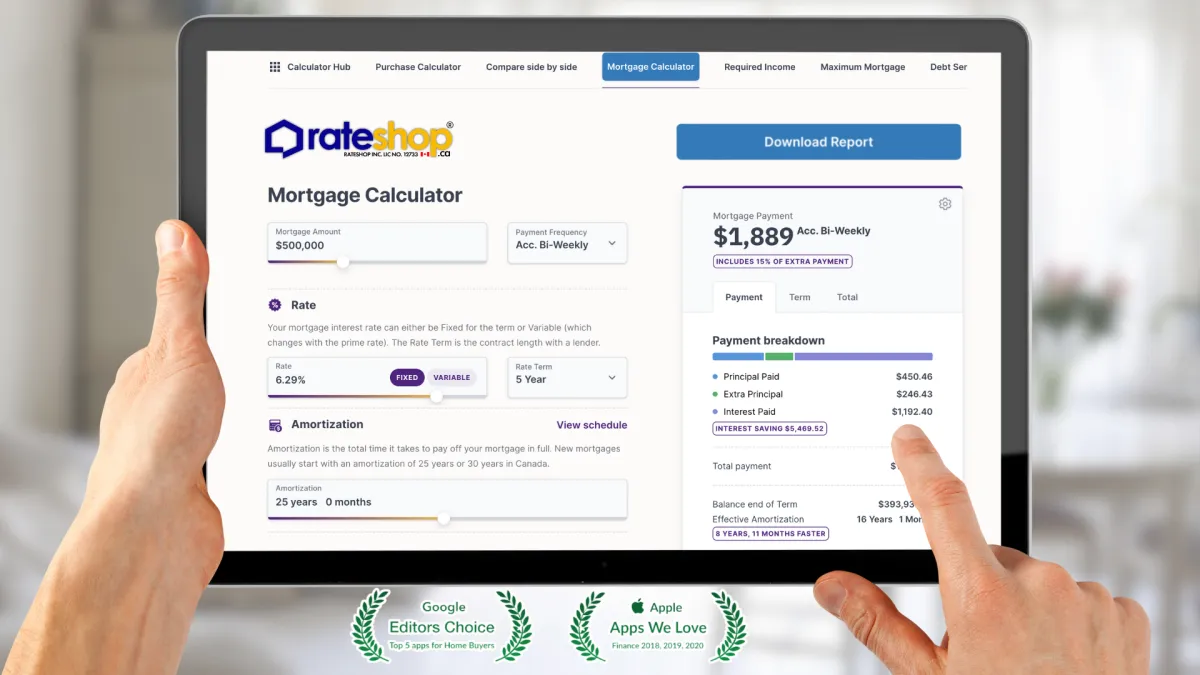

Mortgage Calculator

Easy to use home loan mortgage calculator

Access to Canada's Mortgage Lenders

When you work with RateShop Mortgage, you can access lower mortgage rates than what your bank offers, all while enjoying the same great features like a home equity line of credit or flexible options such as pre-payment privileges.

Our well-connected network of lenders allows us to monitor Canada mortgage lending rates regularly. But we go above and beyond—scouring the internet and collaborating with our lenders to secure better-than-average industry rates. This means deeper discounts and more savings for you.

At RateShop, Canadians gain unfiltered access to the best mortgage rates and home loan rates in Canada. With connections to over 65 mortgage lenders across all provinces, we ensure you get the most competitive mortgage brokering services and broker mortgage loans tailored to your needs.

Whether you’re working with a mortgage broker, exploring mortgage brokerage options, or seeking the expertise of mortgage brokers, RateShop is here to help you find the perfect solution for your home financing goals.

#1 Voted Mortgage Calculators in Canada

Our Mortgage Brokers in Kelowna

RateShop Mortgage Brokers specialize in delivering tailored mortgage solutions designed to help clients secure the best mortgage rates in Canada. With a deep understanding of local real estate trends, particularly in Kelowna, we leverage our expertise in Kelowna mortgage rates to provide the lowest mortgage rates for a variety of property types and financial situations. Whether you’re purchasing, refinancing, renewing, or exploring a home equity line of credit, we work closely with you to compare mortgage rates and lock in the most advantageous deals. Our in-depth knowledge of local lending programs and incentives ensures you maximize your financial benefits.

By tapping into a vast network of lenders, RateShop mortgage brokers help you save on mortgage costs, often securing better deals than major banks like TD, RBC, BMO, and CIBC. We compare Canada mortgage lending rates from over 65 lenders, including banks, credit unions, and monoline lenders, to find low mortgage rates and the best mortgage deals in Canada. This approach allows us to match your unique financial needs with the most competitive home loan rates in Canada, saving you thousands over the life of your mortgage.

Whether you’re working with a mortgage broker, exploring mortgage brokering services, or seeking brokered mortgage loans, RateShop is committed to helping you achieve your home financing goals. From best mortgage rates Kelowna Canada to Canada low mortgage rates, we’re here to guide you every step of the way.

With 1600+ Mortgages Funded, We are Trusted by Canadians

Get Pre-Approved with a mortgage rate hold for 180 days*

Before you Renew with Your Bank, Get a Rate Quote on your Mortgage

Finding the Right Mortgage

Don't lock in just because your neighbor did! Mortgage terms vary from 6 months all the way up to 10 years and you can choose based on your family financial needs. Are you selling soon? Or maybe you want to invest in 2 years. Maybe you want some flexibility, the choice is yours but make it an educated one when you talk to our commission-free mortgage advisors to help you decide on what offers the best mortgage rate and highest savings.

| Fixed Rates | Mortgage Expert Insights |

|---|---|

| 1 Year Fixed Rate |

Great solution for a short-term mortgage needs, renewals can be competitive but rates can go up at maturity without notice. Perfect for new builds to sell after a year or refinance for equity. |

| 2 Years Fixed Rate |

More flexible, a longer duration to support a family need for a couple of years or planning an exit from an existing mortgage without penalties. |

| 3 Years Variable Rate |

3 Year terms can sometimes deliver the best savings, but are typically suggested in a low rate environment, consider a variable too since upon maturity you may get stuck with a higher renewal. |

| 4 Years Fixed Rate |

Banks use this to gain your business, but if you are saving atleast 20-30bps, definitely consider a 4 year term mortgage, compare your savings on a 5 year mortgage term. |

| 5 Years Fixed Rate |

On average, households will upgrade or alter their mortgage about every 5 years, avoiding penalties upon maturity and best rate savings. |

| 5 Years Variable Rate |

Usually recommended in lower rate environments, beat the bank on mortgage penalties and optimize your savings compared to a fixed mortgage offer for the same term. |

Where is the Mortgage Market heading?

History can teach us a lot, check out Canada's mortgage rates history over the past 48 years. Bank of Canada tracks conventional mortgage rates for 3 year and 5 year terms. We can help with understanding the pros & cons to a fixed mortgage rate vs. a variable mortgage rate.

Explore Our Mortgage Options

With recent mortgage rate increases, Canadians are increasingly focused on finding flexible mortgage options that align with their financial goals.

At RateShop, we work closely with our clients to uncover mortgage savings by exploring a variety of offers from multiple lenders. While securing the best mortgage rates in Canada is important, it’s not the only factor in achieving long-term financial stability.

Our experienced mortgage brokers take the time to assess your unique needs, qualifications, and long-term financial goals. Whether you’re looking for home loan rates in Canada, broker mortgage loans, or the best mortgage deals in Canada, we’ll guide you toward the right solution.

By leveraging our expertise in mortgage brokering and access to Canada low mortgage rates, we ensure you get a mortgage that works for you—today and in the future. Let us help you navigate the complexities of mortgage rates and Canada to find the perfect fit for your financial journey!

Learn how to create a monthly income by investing in mortgages

Learn how to create a monthly income by investing in mortgages

About Kelowna, British Columbia

Kelowna, lands at #20 as a top ranking city in Canada in the province of British Columbia and is regarded as a Large Urban population city. In 2021 the Kelowna had a count of 181,380 residents which was a jump of change from the previous census of 2016 where the population size was just 160,095. Kelowna spans over 168.92 km2 and has the #20 rank in population density of 1,073.8/km2.

Kelowna's Real Estate Landscape

Kelowna is a beautiful city in British Columbia, Canada. It is located on Okanagan Lake and is surrounded by mountains. The climate is perfect for growing grapes, and the area is well-known for its wineries. Kelowna is a popular tourist destination, and its real estate market reflects that. Prices are high, but there are still many affordable options available. The market has been steadily increasing for years, and there is no sign of it slowing down anytime soon. If you're thinking of buying property in Kelowna, now is a great time to do so.

Property Use in Kelowna

If you are buying a property to live in Kelowna as a primary residence, also known as a principal residence, then your lowest mortgage rates are guaranteed. Depending on the use of your Kelowna property, certain lenders will price the rate higher if the property is used as a rental investment. Kelowna has a high concentration of primary residences, however there has been an increase in demand for rental properties, mortgage lenders can look at each Kelowna property to determine if the property use was intended as short term or long term rental tenant use.

Our Mortgage Brokers work on approvals from various lenders with specialized investment rental mortgage financing options that include owner-occupied, mixed use or semi commercial properties, some properties with an In-law suite can be used towards an owner-occupied and rental mortgage approval and still qualify for the best mortgage rates. You could be purchasing, refinancing or renewing a mortgage on a Kelowna student rental or a multi-plex property that generates an income and we can still guarantee the lowest mortgage rates.

Canada Mortgage Housing Authority permits the purchase of owner-occupied Kelowna properties with upto 2 units to a 95% loan-to-value and upto 4 units to a 90% loan-to-value.

Best Mortgage Banks, Lenders in Kelowna, British Columbia

Rateshop.ca works with all banks, credit unions and monoline lenders in Canada. With access to so many options, our mortgage broker's focus is on helping you choose a Mortgage Lender in Kelowna, with the lowest mortgage rate offered. We do so by sifting through lenders with promotions in Kelowna. Mortgage lenders may follow their own internal process of financing in your Kelowna.

lenders like TD Bank, Scotiabank, Meridian Credit Union, Duca credit Union and others may have a local branch closest to you in Kelowna. Sometimes the branch facility can cost you a slightly higher rate. In many cases, lenders like First National, MCAP, RMG, ICICI, CMLS, Equitable Bank and others offer a similar suite of services online, even if they don't have a service location in Kelowna. Some Mortgage lenders may also combine additional offers with their mortgage approval as a local customer from Kelowna.

Mortgage Programs Offered in Kelowna

When buying a property in Kelowna, your downpayment determines your eligibility under insured, insurable or uninsured programs.

Insured mortgages in Kelowna start with a minimum of 5% downpayment requirement upto a maxmimum purchase price of $500,000. 10% downpayment is required against the difference between purchase price and $500,000 in addition to the 5% to be eligible for the insured mortgage capped to a purchase price of $1,000,000. The maximum allowed GDS ratio is 39%, and the maximum allowed TDS ratio is 44%. The insurance premium against a default is added to the mortgage amount and amortization is limited to 25 years. These are generally the lowest rates offered by mortgage lenders due to their limited exposure and risk of default.

Insurable mortgages for purchases in Toronto are available through several banks, credit unions and monoline lenders, also known as back-end insured mortgages where the lender will qualify your purchase under a 25 year amortization and limit the GDS ratio to 39%, and the maximum allowed TDS ratio is 44%. However, the downpayment required for this program is a minimum of 20% and the greater the downpayment, better the rate.

For Uninsured Mortgages in Kelowna, the amortization opens up to 30 years, and requires a minimum of 20% downpayment. These rates are higher in comparison to insured and insurable, mainly due to the mortgage lender's own risk towards your purchase. Refinances are typically treated as uninsured. Most mortgage lenders will only offer home equity line of credit products under this program.

In case of Mortgage Renewals, your property in Kelowna can qualify for a lower mortgage renewal rate if you have a low loan-to-value, if you have an active default insurance policy and if you have not changed the amortization on your mortgage since purchase.

To qualify for the right product and lowest rate options, contact our knowledgeable mortgage brokers.

Closing Costs in Kelowna, British Columbia

For any property purchases in Kelowna, you will be required to hire a local Kelowna lawyer to complete the closing. The solicitor's job is to prepare the closing documents according to Kelowna laws and complete the mortgage registration on the property, register the title under your ownership.

The lawyer will perform a title search in the Kelowna of Kelowna database, arrange for title insurance and remit any applicable taxes, in some cases these are Kelowna Land Transfer taxes as well as Kelowna Land Transfer taxes. The lawyer is also responsible for communicating with Kelowna hall to confirm the status of the property taxes to Kelowna. The lawyer will also complete the conditions requested by the Mortgage lenders , and disburse any brokerage commissions on the transaction.

A combination of legal fees, land transfer taxes and registration & title insurance fees are known as closing costs, typically applicable to purchases with exceptions incase to refinances where land transfer taxes may not apply if there are no changes to the title.

Secure Your Dream Home in Kelowna: Find the Best Mortgage Rates and Expert Guidance with RateShop

Impact to My Home Buyers in Kelowna, Canada

For home buyers in Kelowna, fluctuations in interest rates for Canada and Canada mortgage lending rates can significantly impact affordability and purchasing power. Rising rates may reduce the amount you qualify for, making it essential to work with a mortgage broker who can help you navigate these changes. Whether you’re a first-time buyer or looking to upgrade, understanding how mortgage rates and Canada trends affect your budget is crucial.

With home loan rates in Canada on the rise, buyers may need to adjust their expectations or explore alternative options like brokered mortgage loans to secure the best mortgage rates in Canada. A mortgage brokerage can help you compare current mortgage rates in Kelowna to ensure you’re getting the most competitive deal for your situation.

How It Affects Fixed and Variable Rates

The choice between fixed and variable mortgage rates is a critical decision for Kelowna home buyers. Fixed rates provide stability, locking in your interest rate for Canada for a set term, which is ideal for budgeting in a rising rate environment. On the other hand, variable rates fluctuate with the market, potentially offering lower initial rates but with the risk of increases over time.

With Canada low mortgage rates becoming harder to secure, it’s important to weigh the pros and cons of each option. A mortgage broker can help you analyse trends in mortgage rates and Canada to determine whether a fixed or variable rate aligns with your financial goals. For example, if you’re looking for the best mortgage rates Canada 5-year fixed, a broker can guide you toward lenders offering the most competitive terms.

Qualification Process

Qualifying for a mortgage in Kelowna involves several steps, and understanding the process can make it smoother. Lenders will evaluate your income, credit score, debt-to-income ratio, and down payment amount to determine your eligibility. Working with a mortgage broker can simplify this process, as they have access to a wide network of lenders and can help you find the best mortgage deals in Canada.

Getting preapproved for a mortgage is a smart first step. A mortgage loan pre-approval not only gives you a clear idea of your budget but also strengthens your position as a serious buyer. Brokers can also help you explore options like refinancing a mortgage loan or securing a homeowner line of credit if you’re looking to leverage your home’s equity.

Considerations in Finding the Best Mortgage Rate

Finding the best mortgage rates in Canada requires careful consideration of several factors. Here’s what to keep in mind:

Compare Lenders: Don’t settle for the first offer. Use a mortgage brokerage to compare mortgage rates and Canada options from over 65 lenders, including banks, credit unions, and monoline lenders.

Understand Your Needs: Are you looking for the best mortgage rates Kelowna -specific rates? Your location and financial goals will influence the best product for you.

Explore Flexibility: Look for features like pre-payment privileges or the ability to refinance your mortgage if needed.

Work with a Broker: A mortgage broker can help you navigate the complexities of Canada mortgage lending rates and find the lowest Canadian mortgage rate for your situation.

Whether you’re seeking the best mortgage rates in Kelowna, a broker can help you secure a deal that aligns with your long-term financial goals.

Frequently Asked Questions about Mortgages in Kelowna

How to improve your finances with the help of a mortgage?

Consolidate Debt - helps lower your overall interest rate and reduce your monthly payments.

Tax Benefits

Invest in real estate

Use a mortgage to improve your home to increase the value and potentially earn a higher return on investment if you sell it later.

What kind of mortgages are offered in Canada?

Open Mortgage

Closed Mortgage

HELOC (Home Equity Line of Credit)

Reverse Mortgage

Conventional Mortgage

Convertible Mortgage

ARM (Adjustable-Rate Mortgage) or VRM (Variable Rate Mortgage)?

Variable mortgage your mortgage payment amount always remains the same it does not change even if the prime lending rate changes. While adjustable rate mortgage, the amount of your payment changes depending on the prime lending rate.

What mortgage rates are available?

Variable Rates

Fixed Rates

Adjustable Rates

What are today's Best Mortgage Rates?

4.29% - 5 year fixed

5.45% - 5 year variable

You can work with a Rateshop.ca Mortgage Advisors to help you compare options from multiple lenders and find the best mortgage for your needs. It's important to consider not only the interest rate, but also other factors such as the term of the loan, any fees or penalties, the lender's reputation and customer service.

What is a downpayment or Equity?

Downpayment is a payment made by the purchaser when buying a property which means the purchaser's initial investment in purchasing a property. While Equity is the value of your house minus the mortgage amount.

What's included in closing costs?

Closing cost is typically 1.5% of your purchase price. This includes but are not limited to

Land Transfer Tax

Lawyer and Legal Fees

Title Insurance

Mortgage Broker Fee

Property Insurance

What is Mortgage Insurance?

Mortgage insurance is an insurance that protects the mortgage lender or title holder if the borrower fails to make payments, dies, or is otherwise unable to meet the mortgage's terms and conditions.

Everything You Need to Know About Mortgages, Refinancing, and Finding the Best Rates

Portable or Transferable Mortgages

A portable mortgage allows you to transfer your existing mortgage from your current home to a new property while retaining the same terms and interest rates for Canada. This can save you from penalties and help you secure the best mortgage rates in Canada without reapplying.

Standard vs. Collateral Mortgages

Understanding the difference between a standard mortgage and a collateral mortgage is crucial. A standard mortgage uses the purchased property as collateral, while a collateral mortgage includes additional properties, offering flexibility to access more funds. However, collateral mortgages may have higher penalties and are harder to transfer to new lenders.

Steps in a Mortgage Closing

Pre-Qualification: Assess your financial situation to determine how much you can borrow.

Approval: Receive a mortgage offer outlining the terms, including Canada mortgage lending rates.

Conditions & Appraisals: Complete lender conditions and property appraisals.

Solicitor Instructions: Your solicitor receives instructions from the lender.

Signing: Review and sign the mortgage agreement and other legal documents.

Funding: The loan is funded, and the property purchase is complete.

Qualification Criteria

To qualify for a mortgage in Canada, lenders evaluate your income, credit score, and ability to pass the stress test.

Income

Lenders assess your gross debt service (GDS) and total debt service (TDS) ratios, which should not exceed 39% and 44%, respectively. Stable income from salaried jobs is preferred, but self-employed individuals can still qualify with the help of a mortgage broker.

Credit

Your credit score, provided by Equifax or TransUnion, reflects your financial reliability. A higher score can secure you the best mortgage loan rates in Canada.

Stress Test

The mortgage stress test ensures you can afford payments if interest rates for Canada rise. You must qualify at a rate 2% higher than your contract rate or the Bank of Canada’s benchmark rate.

Pitfalls of a Bad Mortgage

Avoid these common pitfalls:

Hidden Fees: Always read the fine print.

High Interest Rates: Compare mortgage rates and Canada to find the best deal.

Prepayment Penalties: Understand the costs of breaking your mortgage early.

Hefty Penalties

Breaking your mortgage early can result in significant penalties, including:

Prepayment Penalties: Charged for paying off your mortgage early.

Discharge Fees: Fees to release your mortgage from the property.

Refinance Restrictions

Refinancing in Canada comes with restrictions:

Maximum LTV: You can borrow up to 80% of your home’s appraised value.

Credit Score: A minimum score of 620 is required.

Income Verification: Lenders will reassess your income.

Appraisal Costs: You’ll need to pay for a property appraisal.

As Seen And heard on

Quick Links

Contact Information

6 Indell Lane, Brampton ON L6T 3Y3, Canada

Local: 416-827-2626

Toll: 800-725-9946

The domain Rateshop.ca is the property of Ali Zaidi operating in Alberta, RECA00523056P. Mortgage applications outside of Alberta may be co-brokered with licensed mortgage strategic partners across Canada. RateShop Inc. is NOT Licensed as a Mortgage Brokerage anywhere except Alberta.

Copyright 2026. Lendmax Capital (Rateshop). All Rights Reserved.