Get Canada's Best Mortgage Rates -

Online & Hassle-Free

Compare rates, calculate your savings, and get pre-approved with expert guidance – serving all provinces, specializing in Ontario, BC, Alberta & Manitoba.

Talk to our Trusted Mortgage Brokers & Get Approved for the Best Mortgage Offers from Banks, Credit Unions & Private Lenders for:

New Home Purchase

Mortgage Renewal & Switch

Refinance & Debt Consolidation

Home Equity Line of Credit

Private 1st & 2nd Mortgage

Commercial Mortgage

USA Mortgage

Canada's Best Mortgage Rates

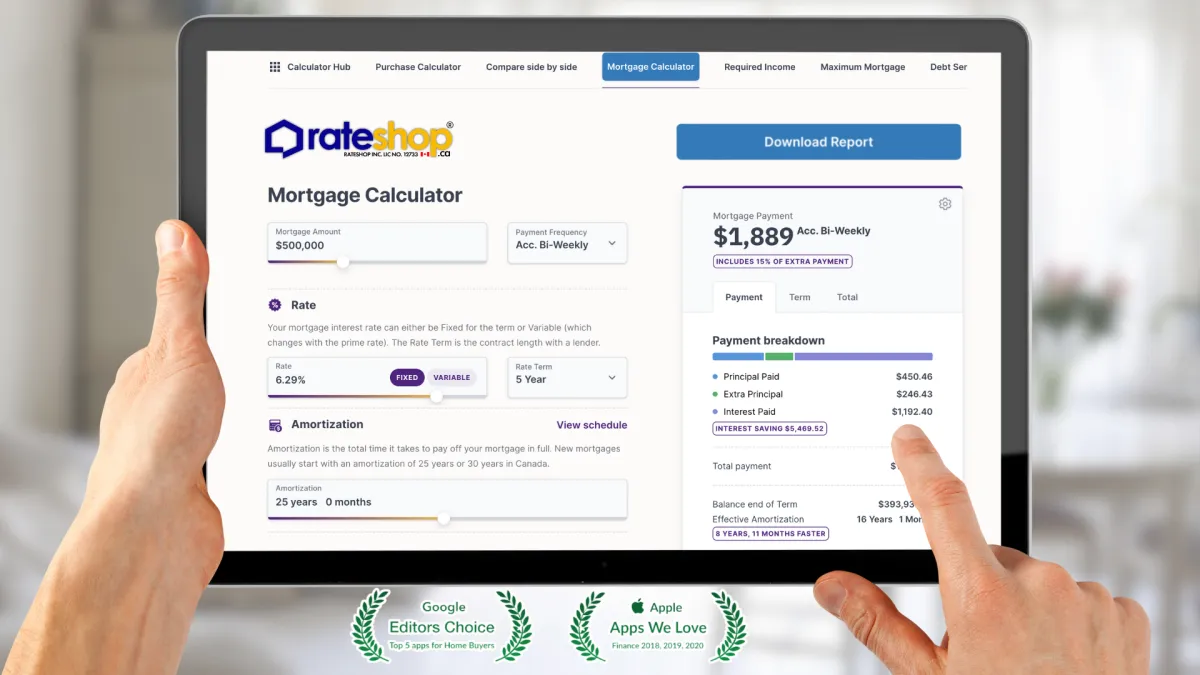

Compare Mortgage Rates & Calculate Your Savings Online

Hassle-free Low Mortgage Rates from

Banks, Credit Unions & Private Lenders

Or Get a Free Rate Quote

1800-725-9946

Start Your Online Mortgage Rate Quote

Access Canada's Largest Mortgage Lender Network

Access Canada's Largest Mortgage Lender Network

Trusted Reviews from Real Customers

See why clients love working with us!

Track Your Mortgage from Application & Funding

Top 8 Reasons To Get Your Mortgage With RateShop.ca

Best Mortgage Rates. Period.

We feature rock-bottom rates from several banks, credit unions, and lenders plus many exclusive low rates that aren’t available through other brokers or lenders directly.

Same Day File Review

Our service commitment is, we will never sit idle on a file. The day we have your application & documents, we start our review immediately to analyze all our lender offers and suggest the best one for you.

Largest Choice of Lenders

We offer the most comprehensive list of banks, credit unions, monoline lenders you’ll find in Canada. More choice, better rates, greater flexibility and dozens of purchase, refinance, renewal & home equity programs.

Easy Mortgage Approval

Our application searches from 700+ mortgage offers with various terms, rate types, and lending programs from 65+ mortgage lenders in Canada, that finds your best suited rate for your unique situation. Unleash the power of Artificial Intelligence to help you save on your mortgage!

Award-winning Service

We work relentlessly to improve every aspect of our service, from service to transparent lending solutions. We’re proud and humbled by our clients' and lenders' appreciation to vote us their preferred partner. Our mission is to provide the best mortgage offerings & services on the planet.

Customers Love Us

We always tell our clients, it's not just about the rate! Finding a solution that works for you, instead of costs you more in the future is what our mortgage planning is about. In two to three years into the mortgage term, this becomes very apparent. Customers have called us back telling us how our advice saved them money and educated them to manage finances better.

Mortgage Lenders Love Us

As a volume broker, our lender relations are important. That's what gets us great rates, and this is possible because we know the programs, we're fluent in underwriting and we are efficient with approvals. Who & What you know in the industry matters, we understand all bank programs and know where to find you flexibility and rate discounts.

Free Mortgage Rate Monitoring

Stay on top of mortgage savings, rate specials, wealth creation tips & investment opportunities. Breaking news affecting mortgage rates and real estate in Canada. We use our AI technology to compare your rate monthly with available lender offers and find the savings for you.

Best Mortgage Rates. Period.

We feature rock-bottom rates from several banks, credit unions, and lenders plus many exclusive low rates that aren’t available through other brokers or lenders directly.

Same Day File Review

Our service commitment is, we will never sit idle on a file. The day we have your application & documents, we start our review immediately to analyze all our lender offers and suggest the best one for you.

Largest Choice of Lenders

We offer the most comprehensive list of banks, credit unions, monoline lenders you’ll find in Canada. More choice, better rates, greater flexibility and dozens of purchase, refinance, renewal & home equity programs.

Easy Mortgage Approval

Our application searches from 700+ mortgage offers with various terms, rate types, and lending programs from 65+ mortgage lenders in Canada, that finds your best suited rate for your unique situation.

Award-winning Service

We work relentlessly to improve every aspect of our service, from service to transparent lending solutions. We’re proud and humbled by our clients' and lenders' appreciation to vote us their preferred partner.

Customers Love Us

We always tell our clients, it's not just about the rate! Finding a solution that works for you, instead of costing you more in the future is what our mortgage planning is about.

Mortgage Lenders Love Us

As a volume broker, our lender relations are important. That's what gets us great rates, and this is possible because we know the programs and are efficient with approvals.

Free Mortgage Rate Monitoring

Stay on top of mortgage savings, rate specials, wealth creation tips & investment opportunities. We use AI to compare your rate monthly with available lender offers and find the savings for you.

Canada's Top Independent Mortgage Brokerage

Compare Rates, Lenders and Your Savings

100% Digital Experience, Guaranteed lowest Rates

Easy Mortgage approvals accross Canada & US*

Unbiased Mortgage Advice to help Financial Growth

Streamlined Funding Guaranteed, You're covered!

5 Star Rated Service with Discounted Online Rates

#1 Voted Mortgage Calculators in Canada

Canada's Best

Mortgage Rates

3.60%

Lowest Purchase

3-YR Fixed

Our Mortgage Experts

Dylan James

Mortgage Agent Level 1

Abdoulaye Sow

Mortgage Agent Level 1

Michael Le Chi

Mortgage Agent Level 1

Heith Gharib

Mortgage Agent Level 1

Sara Fresco

Mortgage Agent level 1

Mortgage Learning Center

2026 Mortgage Renewal FAQs - Updated for Insured & Insurable Mortgages

What you need to know for your 2026 Mortgage Renewal, Frequently Asked Questions:

✅ Question 1: Is the mortgage a Standard or Collateral charge?

If you’re unsure, there are a few ways to validate how the mortgage is registered:

Review the original mortgage documentation

Pull a Purview report to determine if a global limit exists beyond the original mortgage amount

Confirm whether there is a HELOC attached

Pull a copy of the registered charge

As Mortgage Brokers, We have access to FCT’s Broker Portal, where we can access a tool that generates a report confirming how the mortgage is registered (We pay for the fees associated with underwriting your deal).

✅ Question 2: Does the deal meet insurable criteria?

The property value must have been under $1M at the time of the last registration, even if the value is higher you can still qualify under the insured & insurable programs.

This can be validated using:

The appraisal from the previous transaction, or

The purchase and sale agreement if the prior transaction was purchase-based.

If the property value exceeded $1M at last registration but is now under $1M, the deal may be considered on exception:

An appraisal may be required, and both lenders and the insurers must be comfortable relying on the current market value.

The amortization must be 25 years or less. If the am is over 25 years, you can request to scale it down to meet the insurable requirements as well.

✅ Question 3: Can the client qualify at the Contract Rate, or is the Stress Test required?

If the deal is existing default insured, the insurance premium can be ported, allowing the client to qualify at the contract rate.

If the deal is insurable, qualifying at the contract rate becomes more nuanced. All the following conditions must be met:

1. The existing lender must be a Federally Regulated Financial Institution (i.e., a bank). Feel free to reach out to me if you need the FRFI list

2. The mortgage must be fully amortized, with no HELOC or revolving components attached.

3. The amortization cannot be extended as part of the transfer.

If any of the above conditions are not met, the client will be required to qualify under the Stress Test.

✅ Question 4: Can the amortization be extended?

For a standard charge mortgage, the remaining amortization must be calculated as the original amortization minus actual time elapsed.

Example: A 25-year amortization with 5 years elapsed results in a 20-year remaining amortization.

If the client has accelerated payments and the effective amortization is now 18 years, it may be brought back up to 20 years, as this reflects actual time elapsed rather than accelerated paydown.

If the mortgage is registered as a collateral single-charge and meets insurable criteria, the amortization can be re-extended to 25 years while maintaining insurable pricing.

If the deal includes a first and second charge, the mortgages can be merged, and a blended amortization calculated to determine the new remaining amortization.

Cash-flow driven strategy:

A standard charge can be transferred under our New Lender's collateral transfer program to re-extend the amortization up to 30 years.

This would be done at uninsurable (conventional) pricing, and the mortgage must be conventional, with no existing default insurance currently in place.

✅ Question 5: How do you add or remove a Covenant with a Transfers?

Depending on the relationship, it may be possible to add or remove a party from title while maintaining insured or insurable pricing, provided the deal meets the previously outlined guidelines.

Regardless of whether the existing mortgage is a standard or collateral charge, these scenarios are processed as a collateral transfer.

Common examples include:

Removing parents who were acting as co-signers

Adding a spouse or common-law partner to title

FCT will engage a third-party solicitor at a minimal cost to complete the title adjustment and review any land transfer tax implications. This cost can be capitalized within the $3k allotment if there is room

Important limitation: A spouse cannot be removed from title in the case of a matrimonial dissolution.

In these situations, the transaction would need to be completed either as a spousal buyout purchase, where one party is buying the other off title, or as a refinance.

In both cases, a finalized separation agreement must be in place prior to proceeding.

✅ Question 6: How do we mitigate the costs associated with a Transfer?

Our lenders have best costs and strongest transfer programs in the market, particularly when it comes to reducing friction and minimizing our client out-of-pocket costs.

Here’s how we close your deal faster:

Virtual signing through FCT. This option is provided for clients that are computer savvy and is quicker then waiting for an in person visit

Automatic $10,000 buffer added to allow clients to sign prior to receiving the final payout statement. We adjust to the actual balance once the payout amount is then received. We simply do this to place the meeting with FCT prior to the alternative of meeting after the payout is received which is generally just before closing.

From a cost perspective:

Standard transfers: Lenders generally fully covers the transaction cost

Collateral transfers: Costs can be handled in one of three ways:

1. Client pays directly

2. Capitalized within the $3,000 allotment

3. Most popular: We payout of our pocket to help you complete the transfer.

$250 is always added to the payout funds sent to the existing lender to help offset discharge-related fees

If a title adjustment is required, the cost of the third-party solicitor can also be capitalized within the $3,000 allotment, keeping the client out of pocket

We also offer multiple tools within our underwriting to help offset your costs.

Automated Value Method appraisals

Post-funding appraisal rebates on insured and insurable transactions

Minimum $200,000 mortgage is required for the appraisal rebate even though our mortgage lenders will accept a minimum of $50,000 outstanding mortgage balance.

Rebates on the appraisal post funding are up to $400, tiered by mortgage amount

💡 Pro Tip: How to vary the offering and add value

In today’s market, a lot of our clients are seeing available equity has been reduced, clients remain high ratio, or debt restructuring simply isn’t an option. Some of our lenders even offer Cash Back Mortgages as a way to vary the offering and still create meaningful value:

1%, 2%, or 3% cash back built directly into the rate

5% cash back available on conventional deals up to 80% LTV

This can be used to:

Help pay down existing debts, and/or

Offset a prepayment penalty when the mortgage is not yet at maturity

✅ Question 7: What if the current lenders Standard Charge Terms don’t allow for Transfers?

We can circumvent this by doing the deal as a collateral transfer where we can physically discharge and re-register the mortgage. Though the banks won't tell you this to restrict your mortgage transfer options, many mortgages from the banks are setup as a collateral charge under the perception that you can apply for additional credit, however it's more costly to remove the charge and register it again - But you still save more than you would with the bank, and who wants that sneaky approach to hold your equity hostage.

Mortgage Learning Center

First-Time Homebuyer Guide: Getting the Best Mortgage Rates in Canada

Buying your first home is an exciting milestone, but it can also feel overwhelming, especially when it comes to securing the best mortgage rates. With Canada’s diverse housing market and fluctuating m..

Canada's Mortgage Rates in 2025: Trends and Predictions

As 2025 begins, the Canadian mortgage market continues to draw attention, with homeowners, buyers, and investors eagerly anticipating the trends that will shape the housing landscape. Understanding mo...

How to Compare Mortgage Rates in Canada for the Best Deal

When it comes to buying a home in Canada, securing the best mortgage rate is critical to making your investment affordable and financially sustainable. Mortgage rates directly impact monthly payments .

Understanding Fixed vs. Variable Mortgage Rates in Canada

The decision to choose between fixed and variable mortgage rates is one of the most critical choices Canadian homebuyers face.

As Seen And heard on

Quick Links

Contact Information

6 Indell Lane, Brampton ON L6T 3Y3, Canada

Local: 416-827-2626

Toll: 800-725-9946

RateShop Inc. is a Mortgage Brokerage offering lowest mortgage rates to Canadians. We are provincially licensed in the following provinces: Mortgage Brokerage Ontario FSRA #12733, British Columbia BCFSA #MB600776, Alberta RECA #00523056P, Saskatchewan FCAA #00511126, PEI #160622, New Brunswick FCNB #88426, Newfoundland/Labrador.

Copyright 2026. RateShop Canada. All Rights Reserved.